2025 Residential Land Market Report

Market Overview

The 2026 GTA residential land market has entered a more disciplined phase. Activity is being shaped by tighter capital and feasibility constraints, alongside softer housing demand driven more by job-market concerns and uncertainty than demographics. Volumes remain below historical norms, reflecting conservative underwriting and a buyer “wait-and-see” stance - not a loss of long-term confidence. The upcoming CUSMA review and tariff risk add trade uncertainty that can weigh on confidence, delay investment and hiring, and further dampen near-term housing demand and land absorption.

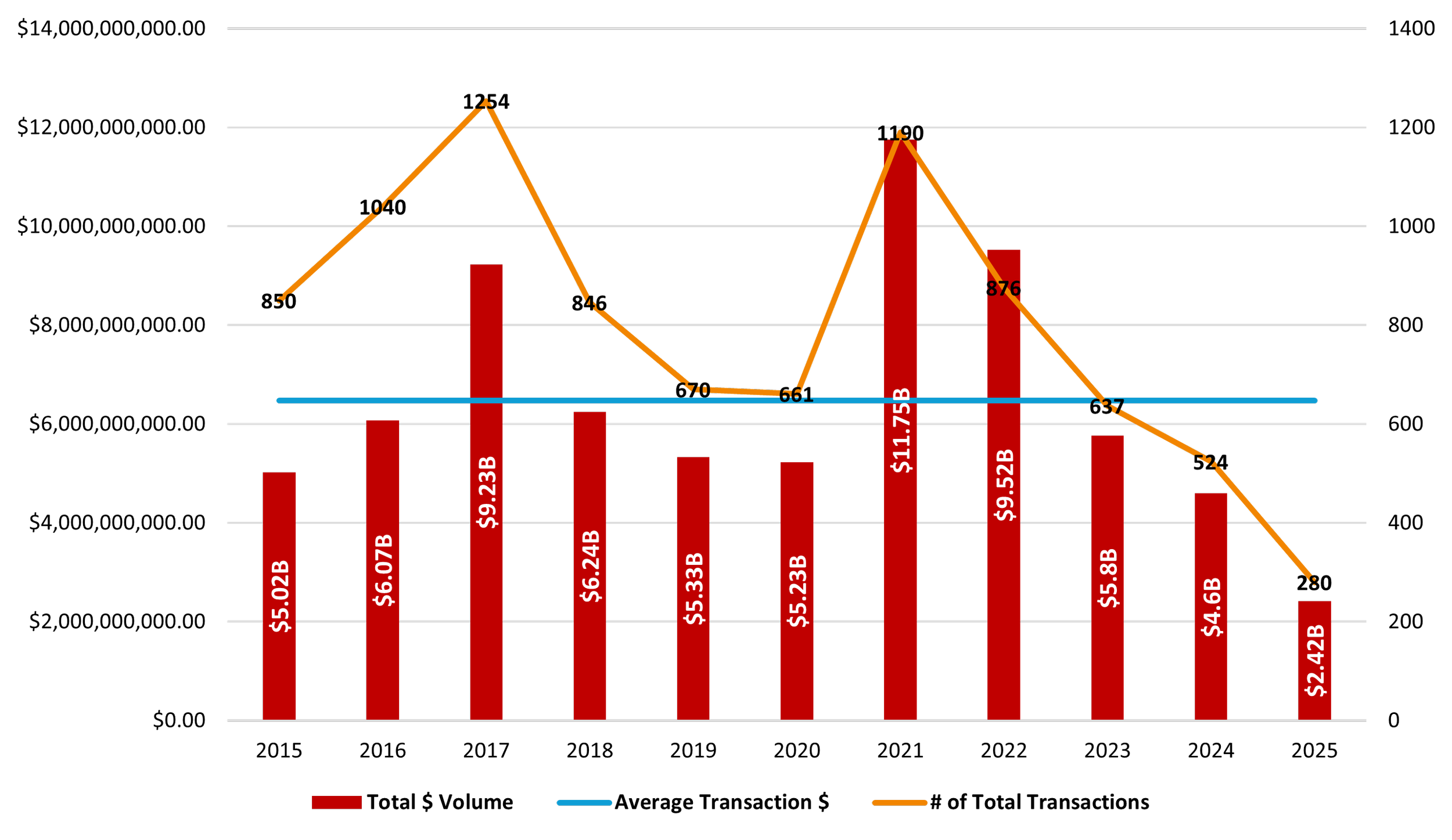

GTA & GGH Residential Land Market

The GTA new home market in 2025 reached what BILD and Altus Group described as "rock-bottom" levels. Total annual sales for the region were approximately 5,314 units, the lowest annual total on record in forty-five years. This represents an 81% decline from the 10-year average of 28,286 sales. This paralysis in the primary market has dictated the movement - or lack thereof - in the residential land sector, where high holding costs and restricted capital access have forced a fundamental shift in developer behavior and project feasibility.

GTA & GGH Residential Land Sales, Annual

The Bifurcation of the Land Market

2025 established a clear divide between "core" land and "fringe" land. Developers are no longer land-banking for the sake of owning acreage. They are selectively acquiring "short timeline" sites with connectivity and affordability. Land that requires a decade-long entitlement process is being devalued, while sites in regions like Durham and Simcoe that can be brought to market within 18 to 24 months command significant interest. Majority of the transactions that happened in 2025 were for land that were designated, had an approved secondary plan or more advanced with Draft of Sub-Division or SPA approved and with services available for development within short timeline.

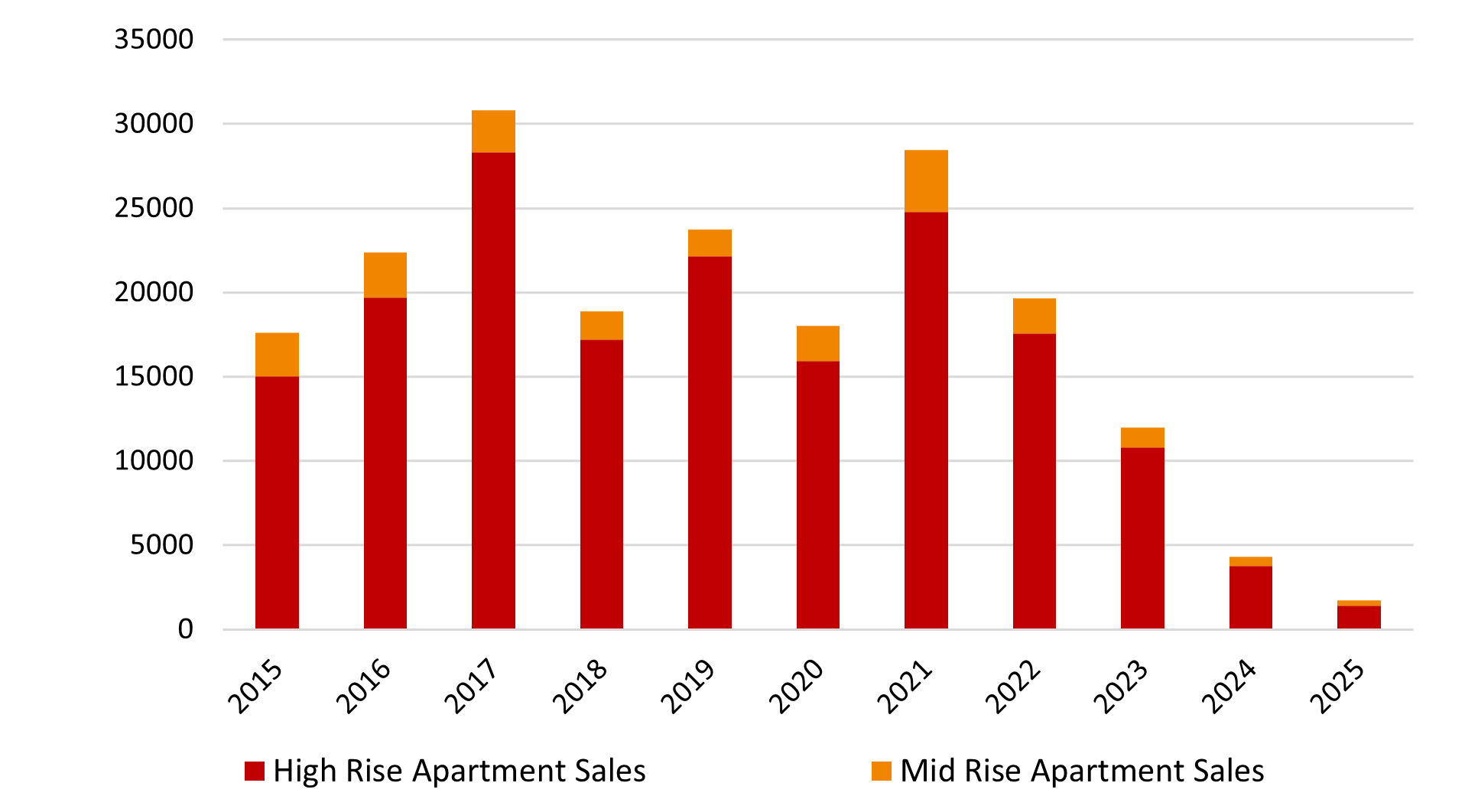

High-Density Land Dynamics

The high-density land segment, which typically supports high-rise condominium development, faced the most severe correction. Bullpen Research and Batory Management reported that high-density land values in the City of Toronto dropped to an average of $92 per buildable square foot in Q2 2025, down 14% year-over-year and 37% from the 2021 peak of $146.

GTA High Density Land Transactions, Annual

The High-Rise Crisis

The high-rise condominium sector bore the brunt of the market stall. Urbanation reported that new condo sales in the Greater Toronto Hamilton Area (GTHA) fell to just 1,599 units in 2025, a 60% drop from 2024 and 91% below the 10-year average. By Q4 2025, quarterly sales reached their lowest point since 1990.

Feasibility issues were the primary driver of this decline. A "negative cash flow" scenario effectively removed investors, who typically account for 70% or more of pre-construction sales, from the market. Project cancellations spiked to record levels in 2025. A total of 28 active new condominium projects, representing 7,243 units, were cancelled - more than double the units cancelled in 2024.

GTA Pre-Construction Apartment Sales

Overall, the market has become more selective, not inactive. Land is trading where pricing, timing, capital structure and affordability of the end product based on household income align. Heading into 2026, value will continue to favor certainty, speed to market, and alignment with end-user affordability.

For further reading: