2025 ICI & Industrial Market Report

Market Overview

2025 has redefined the "rules of the game" for industrial building and land sales in Canada. The convergence of the "Productivity Super-Deduction," Ontario’s Special Economic Zones, and the massive build-out of the Ring of Fire infrastructure has created a policy environment that favors long-term, high-value manufacturing over short-term logistics speculation.

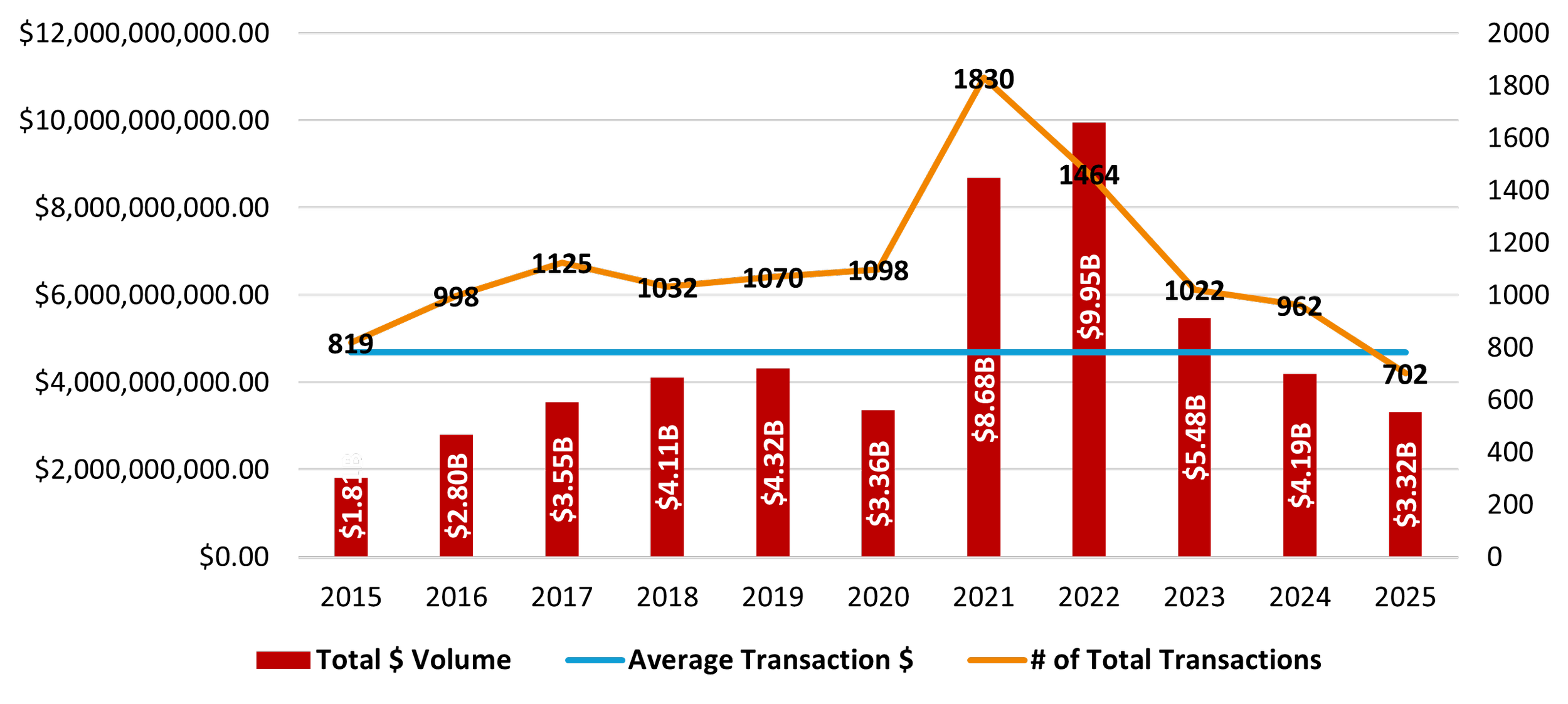

ICI Land Sector

The industrial market backdrop at the end of 2025 helps explain why ICI land activity across the GTA and GGH remains restrained. After much of the year marked by hesitation, Q4 delivered a modest improvement, with net absorption rebounding to just over 4.1 million square feet, the strongest quarterly result since late 2022. Leasing momentum was driven primarily by third-party logistics users and a handful of large-bay transactions. However, this pickup was largely offset by a similar volume of new supply deliveries, nudging availability higher to 4.6 percent and reinforcing that the market is stabilizing, not tightening.

Pricing and development conditions continue to pressure both occupiers and landowners. Asking net rents declined again in Q4 and are down roughly six percent year-over-year, reflecting increased competition, more second-generation space, and growing tenant leverage. These dynamics, combined with elevated construction costs and more conservative lending, have slowed the development pipeline materially compared to recent years. While this slowdown should help restore balance longer term, near-term risk remains concentrated in submarkets with heavier recent deliveries and higher exposure to speculative product.

GTA & GGH ICI Land Sales, Annual

Key ICI Market Trends

Industrial leasing has improved modestly, but remains fragile and supply-driven

Availability is rising as new deliveries outpace sustained demand

Asking rents are trending down, resetting development and land value expectations

Construction activity is slowing, which should support longer-term balance

Capital remains selective, favouring serviced sites and near-term execution over speculation

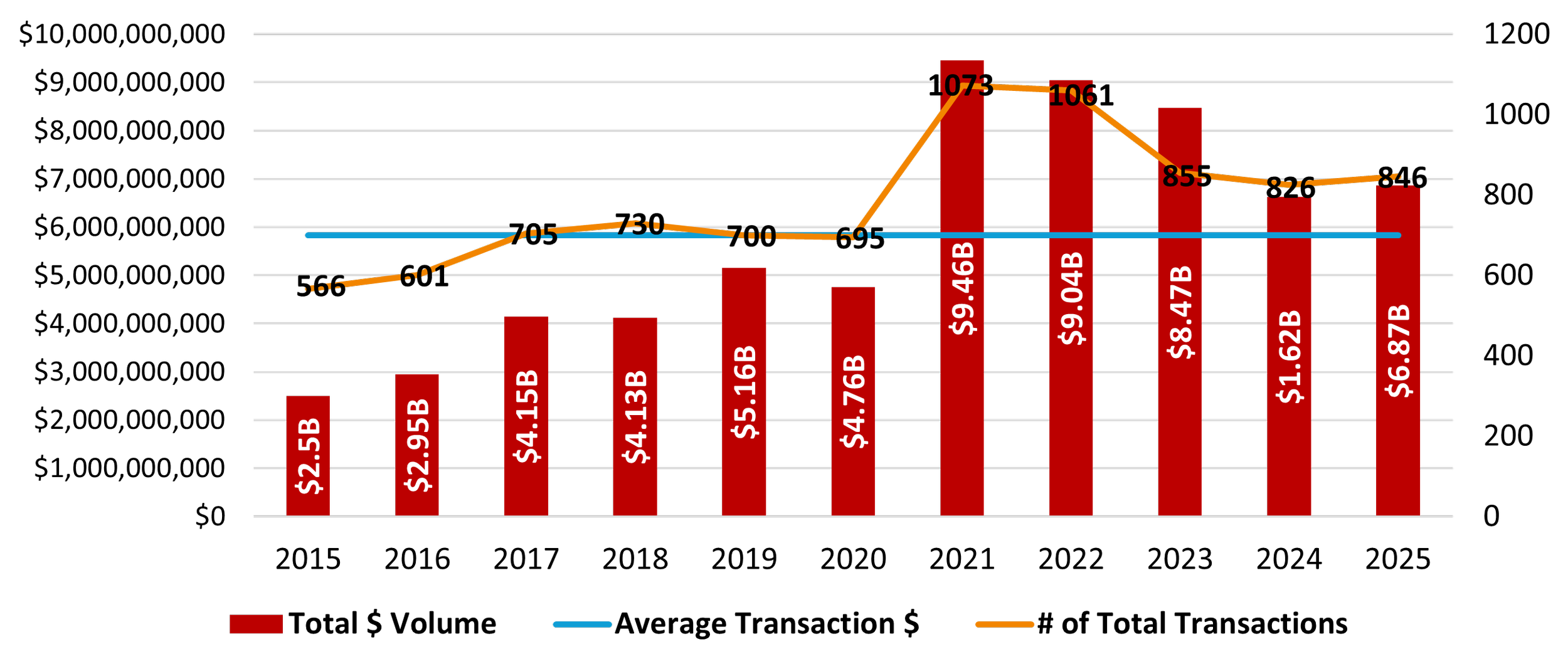

Industrial Building Sector

Industrial fundamentals across the GTA are normalizing after the post-COVID expansion cycle. Vacancy has risen from a historic low of 0.8% in late 2021 to 4.4% today, driven by speculative supply delivering ahead of demand. Availability has climbed further to 6.5%, reflecting slower leasing from 3PLs and increased caution tied to tariffs and trade uncertainty. Submarkets that saw the most aggressive development, particularly GTA East and North GTA West, are experiencing the greatest softness.

GTA & GGH Industrial Building Sales, Annual

Key Industrial Building Takeaways

Vacancy has risen to 4.4% as speculative supply outpaces demand

Rents have turned slightly negative and are expected to remain flat near term

Investment liquidity remains strong, despite pricing adjustments

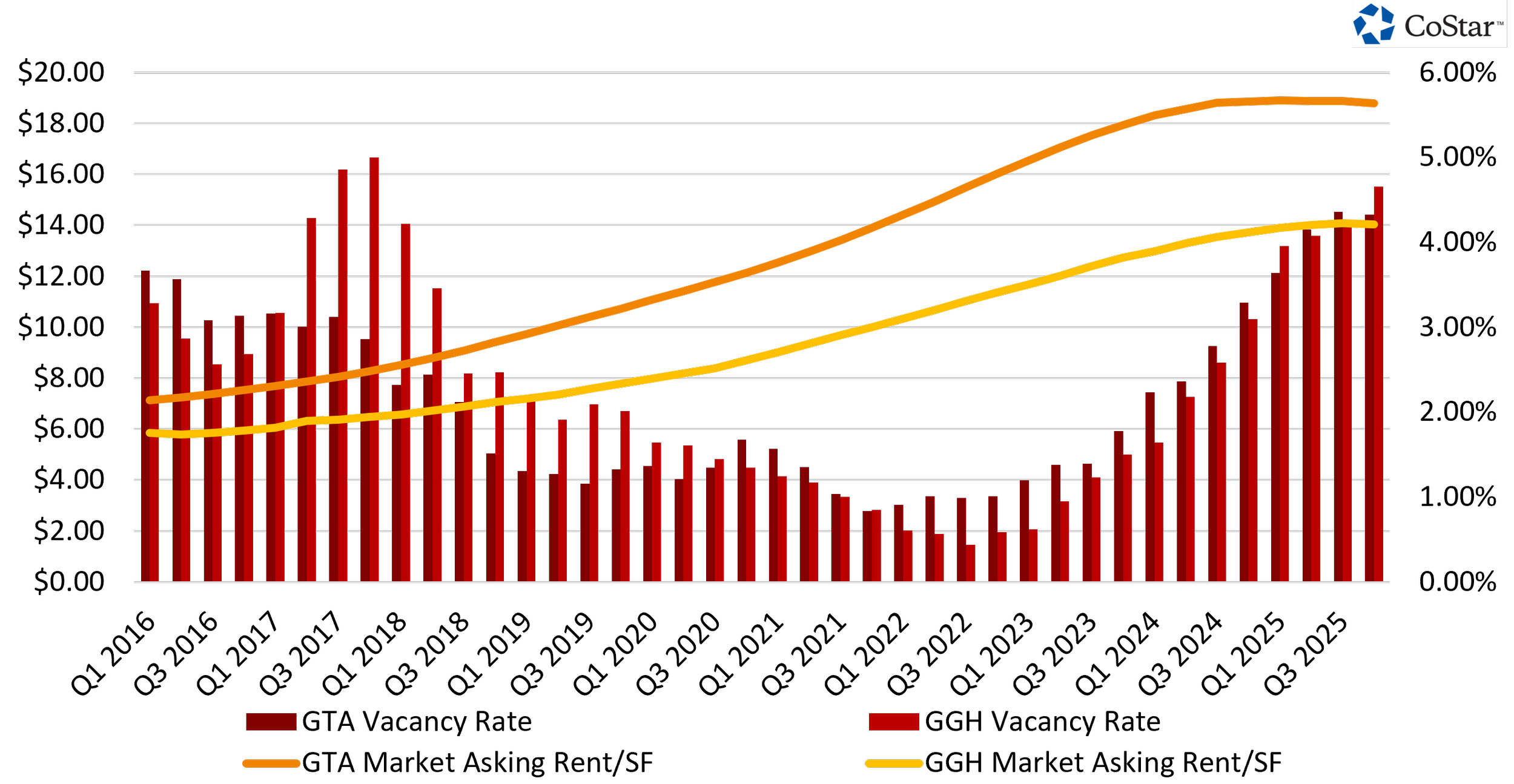

Industrial Leasing

Leasing conditions across the GTA in 2025 reflect a market still searching for firm footing after the post-pandemic reset. While activity has stabilized compared to the sharp pullback seen through 2023 and early 2024, momentum remains fragile. Vacancy has climbed to 4.4%, well above historical norms, as new supply continues to outpace demand. Much of today’s leasing activity is driven by renewals rather than expansion, with occupiers hesitant to commit amid tariffs and escalating trade tensions. Rising availability, now at 6.5%, is increasingly influenced by sublet space concentrated in older buildings, pointing to a growing flight to quality as tenants gain negotiating leverage and rents soften.

GTA & GGH Vacancy & Market Asking Rent per SF

Key Takeaways

Leasing is dominated by renewals as new deal activity slows amid economic and trade uncertainty.

Vacancy and availability continue to rise as new supply and sublet space hit the market.

Sublet space is largely concentrated in older buildings, driving a clear flight to quality.

Modern, large-scale logistics facilities remain competitive and continue to attract major tenants.

Market conditions have shifted in favor of tenants, with increased choice and leverage.

For market participants, the GTA remains a region of relative stability, yet the "standstill" of 2025 has given way to a more disciplined, bifurcated market where quality and "cash flow is king". The cooling of population growth and the threat of U.S. tariffs are real headwinds, but they are being met with a level of government fiscal and regulatory intervention not seen in the post-war era.

As the St. Thomas gigafactory takes shape and the Greenstone Transmission Line begins to stretch northward, the Canadian industrial sector is no longer just reacting to global trends, it is actively attempting to build a self-reliant, vertically integrated future. The successful navigation of this "new frontier" will require industrial owners and developers to be more than just land managers; they must be strategic partners in a national project of economic sovereignty.

For further reading: