2025 Retail Market Report

Market Overview

The 2025 retail year in the GTA was defined by the death of the "middle." The insolvency of Hudson’s Bay was the final capitulation of a retail model that no longer served the modern Canadian consumer. However, the speed with which the market pivoted expanding luxury at one end and discount at the other demonstrates the underlying dynamism of the Toronto region. The 2025 GTA retail landscape is characterized by limited supply in prime nodes and a strategic shift toward experiential tenants. Vacancy rates in Super Regional malls remain historically tight.

Retail fundamentals across the Greater Toronto Area remain resilient, supported by a decade of strong population growth and limited new supply. From 2016 to 2024, population growth far outpaced retail inventory expansion, keeping vacancy tight and the market largely landlord-favourable. Momentum is slowing, however. Population growth is expected to decelerate, with forecasts pointing to a potential decline in Toronto in 2026, and broader economic uncertainty on the horizon.

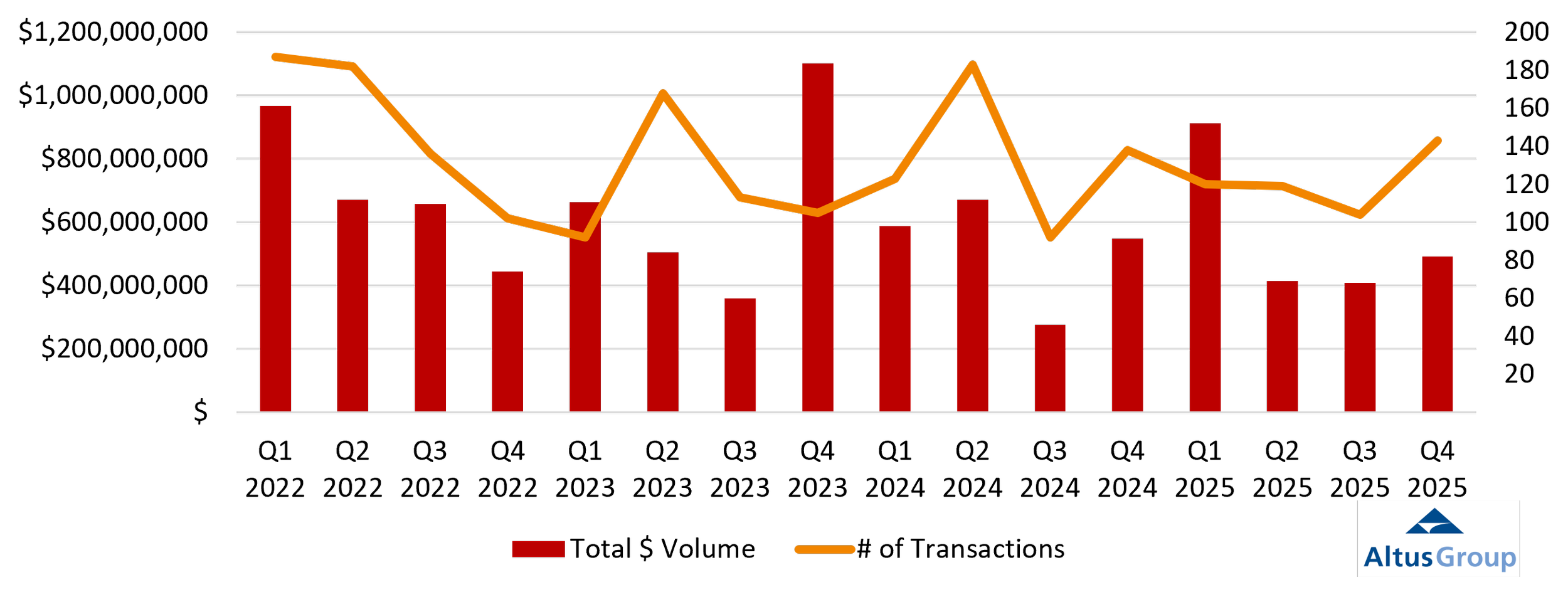

GTA Retail Sales

For 2025, we finished at $3.6 Billion in total dollar volume and a total of 739 transactions, which was above the 10 year average dollar volume with higher transaction value.

Rental growth has flattened; recent trades highlight investor preference for stabilized, needs-based retail. While macro-level risks grow with unemployment expectations from Oxford Economics and weakening consumer sentiment from Bank of Canada, daily-needs retail remains well-positioned. Shifting trade dynamics and higher tariffs on imported goods could favour domestic retailers with local supply chains, positioning brands such as Canadian Tire, Indigo, and LCBO to benefit from renewed interest in brick-and-mortar shopping.

Retail Building Sales

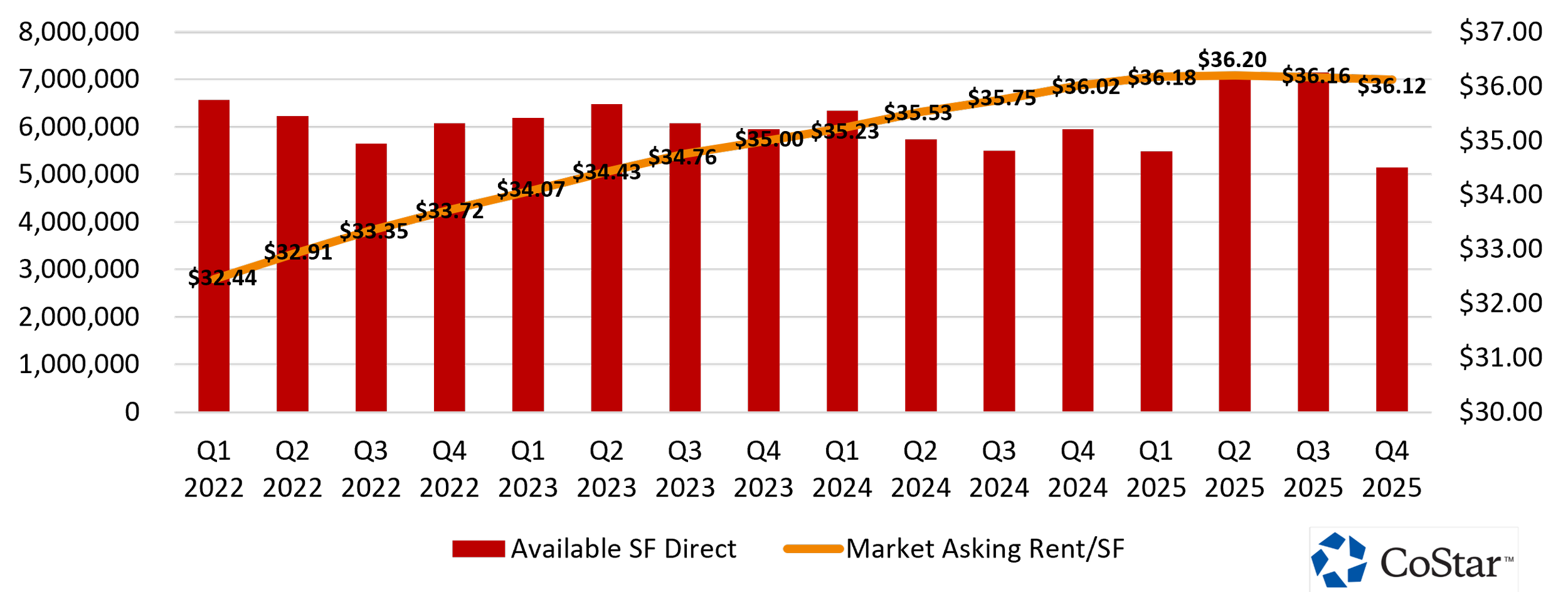

Estimated Asking Rate

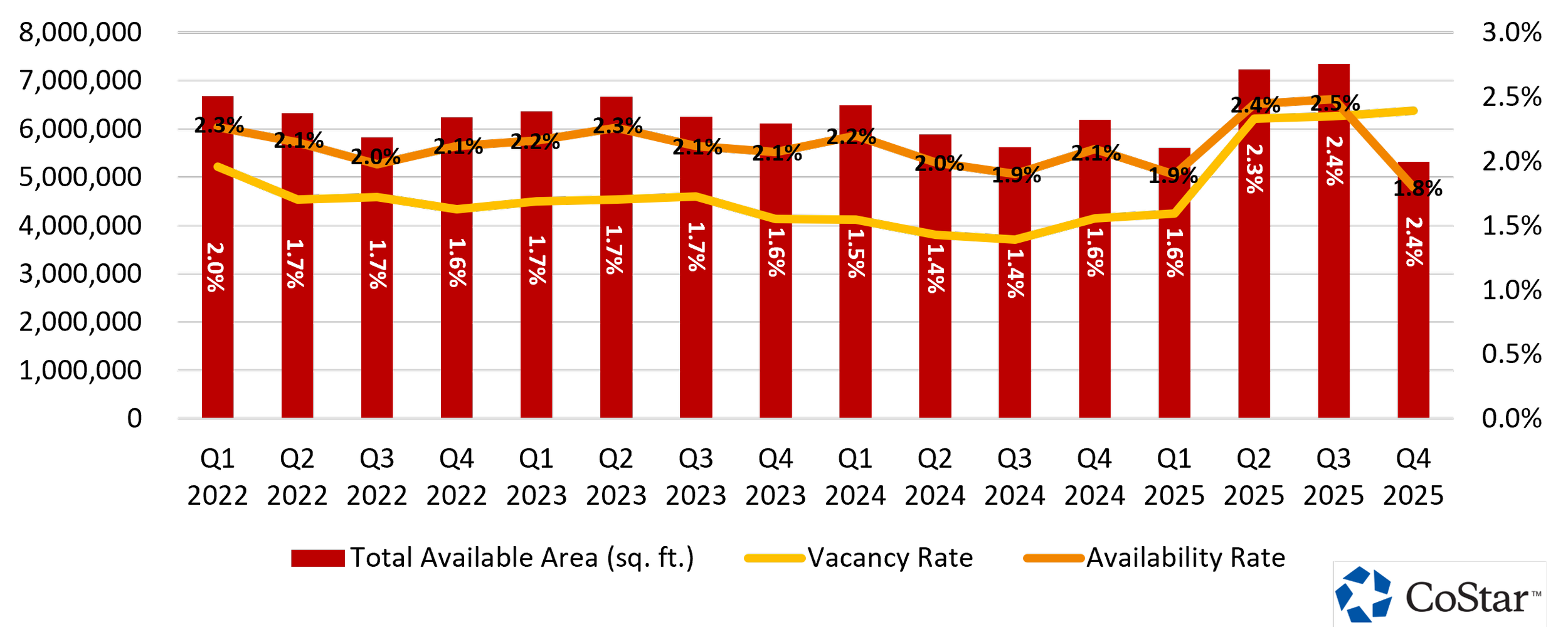

The most notable disruption has been the nationwide closure of Hudson's Bay Company, which pushed GTA retail vacancy up to 2.4% and drove negative net absorption for the first time in a decade. Large-format mall space has been most affected, while neighbourhood and necessity-based retail continues to perform well particularly in suburban areas like the northwestern GTA where vacancy remains below 1%. New construction is modest at just 0.2% of inventory under way, as high costs and the reintroduction of anchor space temper developer appetite.

Vacancy & Available Lease Rate

Key Takeaways

Negative absorption is largely attributable to HBC anchor closures

New supply is limited, with only 0.2% of inventory under construction

Rental growth has stalled, with downside risk in the near term

Investor demand remains focused on stabilized, needs-based retail assets

Domestic retailers may benefit from trade-related pressures on cross-border e-commerce

OpEx Pressure: Retailers faced increasing operating expenses, driven by wage growth and logistics costs. This pressured margins for low-volume retailers, accelerating the exit of undercapitalized brands

The Consumer Bifurcation

Households in the GTA faced significant headwinds in 2025, primarily due to the wave of mortgage renewals at higher interest rates. This reduction in discretionary income for the mass-affluent demographic devastated the "aspirational middle" retail segment.

For further reading: